Welcome to The Contrabass Shoppe

Based in the UK, we specialise in the sale of professional quality old double basses and bows. Passionate about the double bass, we offer instruments of unquestionable authenticity and structural soundness.

Top Quality Basses

Bows

Quality Basses

More About Us

In addition to being recognised as the 'Numero Uno' for professional quality double basses in the UK, The Contrabass Shoppe has gained an enviable global-reputation for the meticulous presentation of their instruments and the outstanding qualities of sound and tone that they induce from each double bass in what is a sizeable inventory.

As a former member in the double bass section of the London Philharmonic Orchestra, Director Anthony Houska knows exactly how a good instrument should sound, feel and look.

Testimonials

"Congrats for the astonishing, breath-taking and flabbergasting collection of basses and bows."

"Nowhere else did I encounter such excellent service."

"Your business is well run and honest about identifying the strengths and weaknesses of each double bass."

Instrument Reviews

H. R. Pfretzschner French Double Bass Bow With Additional German Style Frog In 14ct Gold – Review

Can you tell me a little bit about this bow? Yes - this is a fairly typical but at the...

5-String Double Bass by Neuner & Hornsteiner, Mittenwald anno 1877 – Review

We are looking for a good 5-string instrument but there doesn't seem to be many available on the market -...

Cremona School Double Bass by István Kónya, Hungary anno 1983 – Review

What is the Cremona School? The Violin Making International School of Cremona was founded on 21st September 1938 The aims...

H. R. Pfretzschner French Double Bass Bow With Additional German Style Frog In 14ct Gold – Review

Can you tell me a little bit about this bow? Yes - this is a fairly typical but at the...

5-String Double Bass by Neuner & Hornsteiner, Mittenwald anno 1877 – Review

We are looking for a good 5-string instrument but there doesn't seem to be many available on the market -...

Cremona School Double Bass by István Kónya, Hungary anno 1983 – Review

What is the Cremona School? The Violin Making International School of Cremona was founded on 21st September 1938 The aims...

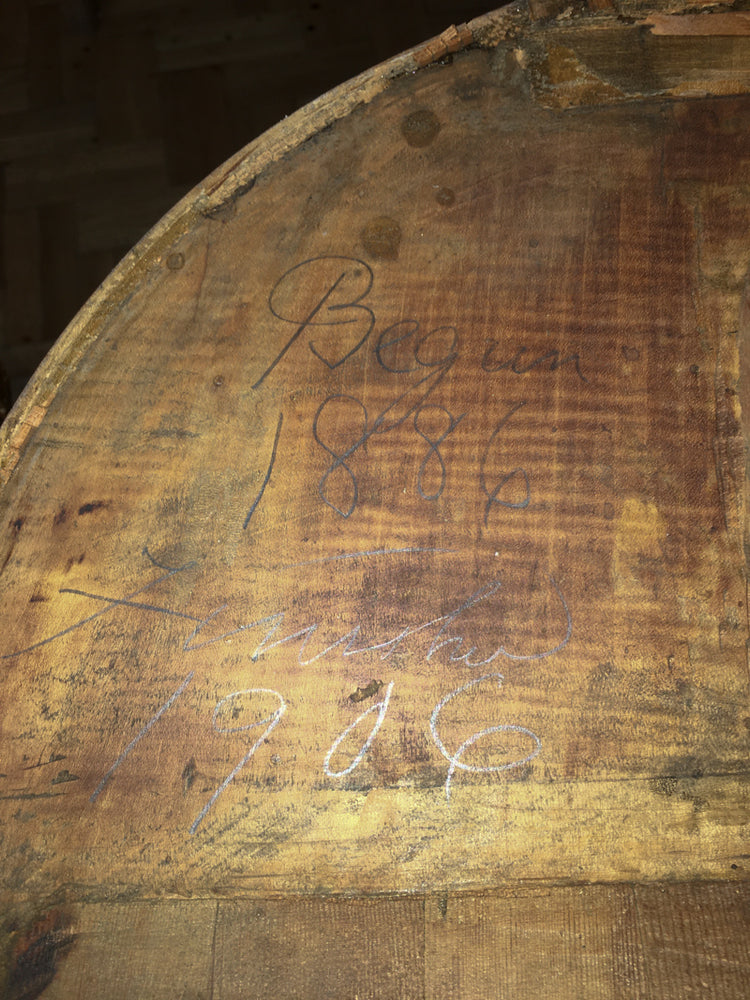

Double bass by Thomas Calow, Nottingham anno 1886

This interesting and incredibly rare instrument bears the pencil inscription on the upper back that it was started in 1886 when Thomas was aged 18 and following his premature death in 1905 finished off by his father and brother in 1906. This testimony is supported by the fact that the former neck-block bore the brand F. Calow, Nottingham. The 20 years to complete, quite probably setting a world record for the longest completion of any stringed instrument if not any type of musical instrument. Even more incredible is the fact that Barry Young, who was the former principal of Northern Ireland`s Ulster Orchestra for an unprecedented 41 years had used the instrument as his main companion just as he had purchased it himself - setup with its original hand-made “footless” bridge still fitted! The original Calow, Nottingham branded bridge to have remained fitted for + or - 130 years quite possibly setting another world record.

The instrument has recently undergone an extensive-rebuilt that has given it poise, balance and grace and the largest and most punchy sound imaginable. For those investors wanting even more provenance, the instrument is featured in full colour on pages 96-97 of the exquisitely produced publication entitled The English Double Bass by Thomas Martin, Martin Lawrence and George Martin.

Stats:

LOB (length of back) - 115.3cm (45.39in)Width across upper bouts - 50.7cm (19.96in)

Width across middle bouts - 37.6cm (14.80in)

Width across lower bouts - 68.0cm (26.77in)

Depth of lower ribs inc both plates - 20.8cm (8.19in)

Body Stop - 60.7cm (23.90in)

String length - 105.6cm (41.57in)

Reference number #2895